Schedule a Call Back

Energy Shocks Threaten Global Manufacturing Stability

Articles

Articles- Mar 24,26

Rising energy costs and supply chain disruptions linked to the Strait of Hormuz are set to impact global manufacturing, driving cost pressures, production challenges and weaker industrial investment.

Key Takeaways

- Prolonged Strait of Hormuz disruptions will sharply raise energy and freight costs, hitting chemicals, metals, and export-driven manufacturing first.

- With no post-Covid buffer, rising input costs are likely to delay capex, reduce machinery demand, and weaken global manufacturing growth.

The ongoing US–Iran conflict and its aftermath are expected to trigger delayed shipping, energy instability and supply chain disruptions, with significant knock-on effects on the global manufacturing economy.

The Strait of Hormuz accounts for roughly 20 per cent of global liquid natural gas (LNG) trade and up to a quarter of seaborne oil. Disruptions have driven energy futures higher, with Atlantic and Pacific LNG freight rates rising by over 40 per cent. South Korea’s maritime ministry has advised shippers to avoid operating in the Middle East, while maritime data indicates a nearly 70 per cent drop in traffic by 28 February 2026, alongside increased risks of force majeure and liability exposure.

Historically, similar disruptions—such as the 2021 Suez Canal blockage—have impacted logistics, while the Russia–Ukraine energy shock continues to influence energy prices and European manufacturing. The current situation combines elements of both, with parallels to the 2015–16 industrial slowdown.

The manufacturing impact is expected across three areas. Energy-intensive sectors, including chemicals and metals, are likely to face rising costs. Export-driven manufacturing hubs in Asia may encounter higher input costs and freight disruptions due to reliance on Gulf petrochemicals. Sustained energy price increases could also weaken machinery and industrial equipment demand as manufacturers delay or scale back investments.

In 2022, the post-Covid manufacturing rebound masked Europe’s exposure to energy shocks. With this buffer now diminished, similar disruptions today could produce more pronounced effects.

Energy Shock Impact

Energy market disruptions and constrained shipping routes typically impact manufacturing through supply chains. Energy-intensive production is affected first, followed by broader industrial investment decisions. While the 2022 Russia–Ukraine energy shock did not immediately reflect in output data due to strong post-pandemic demand, sector-level analysis shows significant strain.

Fig 1

In Germany, energy-intensive industries such as chemicals and metals faced considerable cost pressures. Although growth persisted during the recovery phase, it was largely driven by economic normalisation rather than sustained industrial momentum. By 2023, these sectors contracted, with the chemicals and pharmaceuticals sector shrinking by 14.4 per cent—exceeding its pandemic-era decline.

Fig 2

A clearer historical comparison is the 2015–16 industrial slowdown, when oil market shifts and weakening demand reduced manufacturing activity and industrial investment. Although energy prices fell during that period, the transmission mechanism—where energy disruptions influence investment cycles—remains comparable.

If disruptions in the Strait of Hormuz persist, the resulting impact may resemble the 2015–16 slowdown more than the 2022 crisis. Without the support of a post-Covid recovery, rising energy costs could directly affect production levels. Higher costs for manufacturers and consumers are likely to reduce industrial investment and weaken machinery demand.

Fig 3

With order backlogs normalised, inventory cycles stabilised and industrial growth slowing, the current manufacturing environment is more exposed. Prolonged disruptions to energy supply or shipping routes could directly impact production and investment, potentially leading to a significant downgrade in global manufacturing outlook.

Fig 4

What this means now

Historical data indicates that disruptions to energy markets and shipping routes propagate predictably through manufacturing. Unlike 2022, when recovery momentum cushioned the impact, current conditions suggest greater vulnerability. Sustained disruptions—such as those affecting the Strait of Hormuz—are likely to result in higher input costs, production pressure and reduced industrial investment.

Why manufacturing intelligence matters

Understanding how these disruptions affect sectors is critical for identifying risks and opportunities. For manufacturers, suppliers and investors, visibility into sector-level trends is increasingly important. Tools such as the Manufacturing Industry Output Tracker enable analysis of how energy volatility, supply chain disruptions and macroeconomic shifts influence the manufacturing economy.

About the author:

Jack Loughney, Senior Data Analyst, Interact Analysis works as the primary data analyst across multiple research activities. His expertise lies in data modelling, economic forecasting and streamlining processes to enhance product efficiency. Jack is responsible for the upkeep and enrichment of our MIO tracker.

global manufacturing

energy shock

supply chain disruption

Strait of Hormuz

industrial investment

LNG trade

energy prices

manufacturing outlook

US Iran conflict

Jack Loughney

Interact Analysis

Related Stories

Machine Tools & Accessories

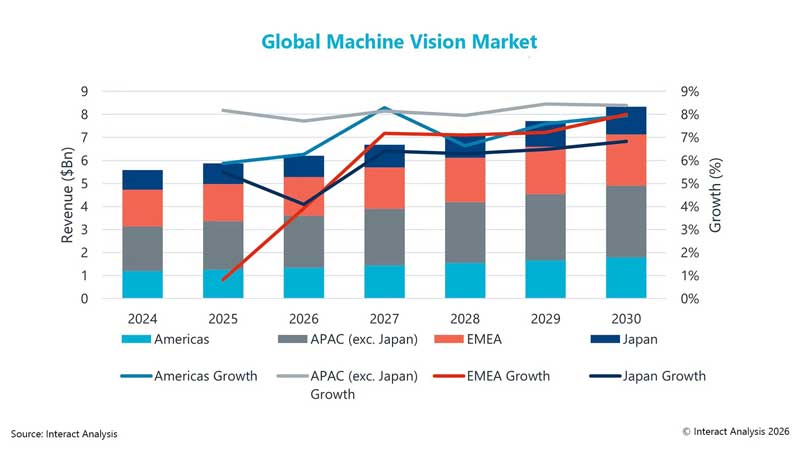

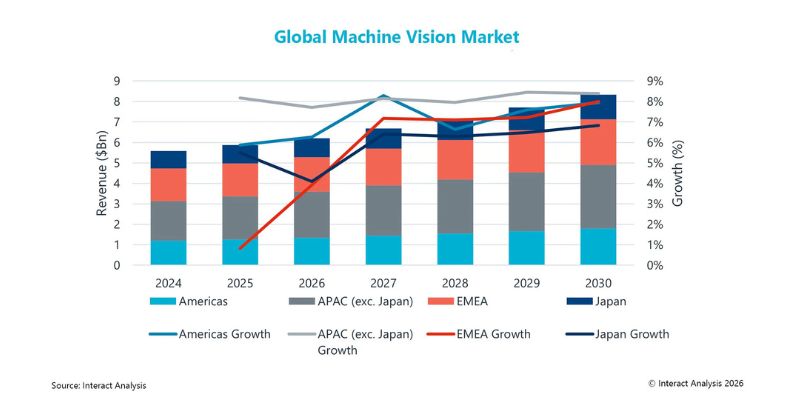

Machine vision market set to reach $8.3bn by 2030: Interact Analysis

Machine vision is set for steady growth, driven by 3D cameras, vision software and logistics automation, as demand for precision inspection rises across industries despite tariff pressures

Read moreSmart Manufacturing

Machine vision industry will reach $8.3bn in 2030: Interact Analysis

Interact Analysis says machine vision grew 5.2 per cent in 2025 and is forecast to expand 7.2% annually to $8.3 billion by 2030, driven by 3D cameras, software and logistics automation.

Read moreSmart Manufacturing

Is on-premise warehouse software making a comeback?

Rising AI workloads, cloud cost concerns, cybersecurity risks and data sovereignty requirements are prompting warehouse software buyers to reassess on-premise deployments, even as cloud remains the ..

Read moreRelated Products

latest News

Subscribe to iNoW

For Industry News on WhatsApp, Give a Miss Call on: +91 84228 74016