Schedule a Call Back

Top 30 manufacturers account for 84% of global geared motors market

Articles

Articles- Mar 21,25

Industrial reducers and gearmotors have formed a stagnant market landscape after a long period of development. Interact Analysis’ report found that the global sales rankings of the top 30 manufacturers remained relatively stable between 2023 and 2024, says Shirley Zhu, Prinicpal Analyst, Interact Analysis.

After three consecutive years of growth, the global geared motors and industrial gearbox market experienced a 3.7% year-on-year decline in sales in 2024, dropping to $12.4 billion, according to our Geared Motors and Industrial (Heavy-duty) Gears – 2025 report. All tri-region markets (Asia Pacific, Europe, Africa & the Middle East, and the Americas) suffered sales declines of varying degrees, due to constraints such as weak downstream demand and de-stocking processes. Consequently, leading market players have increased their market share, thanks to their competitive advantages in product technology, distribution channels, and brand recognition – leading to a more concentrated market landscape.

Top 30 gearbox manufacturers accounted for 84% of market share

Industrial reducers and gearmotors (traditional and mature industrial automation products) have formed a relatively stable market landscape after a long period of development. Interact Analysis’ report found that the global sales rankings of the top 30 gearmotor and industrial gearbox manufacturers remained relatively stable between 2023 and 2024. Their combined revenue accounted for an estimated 84% of total global market revenue in 2024, an increase of one percentage point compared with 2023. The performance of these suppliers reflected the overall market situation during these two years. In 2023, major Asian suppliers underperformed, compared with their counterparts in the EMEA and Americas regions. In 2024, most of the top 30 suppliers experienced varying degrees of revenue decline. Compared with suppliers in the Americas region, those in the Asia-Pacific and EMEA regions were more severely affected.

European manufacturers still dominate the global gearbox market

The top 30 gearbox manufacturers (based on market share) are geographically segmented across the tri-region: 15 have their headquarters in Europe, 10 are in the Asia Pacific region, and four are in the Americas. The prominent position of European suppliers is not only reflected in their dominance in the European market but also in their significant market shares in the American and Asia Pacific markets. The landscape of geographical distribution for leading gearbox vendors is closely related to the industrial base, the gearbox development history, and the market demand of each region.

Most of the top 30 suppliers experienced varying degrees of revenue decline in 2024

Due to its strong industrial heritage, Europe has been a leader in fields such as machinery and automotive manufacturing, driving the local development of gearboxes. Take Germany, for example. Its high-precision machinery manufacturing technology is recognised as advanced globally, with substantial technical capabilities in the fields of industrial gearmotors and gearboxes. This has enabled local suppliers to occupy dominant positions in the global market with high-performance products. Our data shows that, among the world’s top 30 gearbox manufacturers, the leading enterprises in the Americas and Asia Pacific regions still focus their sales on domestic markets. Although there are numerous suppliers in the Asia Pacific region (excluding Japan), due to its relatively late start in gearbox development it still needs to make breakthroughs in core technology research and development, and brand building. However, rapid development of the region’s manufacturing industry development over the years has driven a continuous increase in demand for industrial geared motors and gearboxes, providing huge growth for local enterprises.

Leading manufacturers offer diverse product ranges

From the perspective of product types, most of the top 30 gearbox suppliers offer a wide variety of geared motors and industrial gearboxes, spanning two to three product categories (light-duty geared motors and gearboxes, heavy-duty industrial gearboxes, and planetary geared motors and gearboxes). Light-duty gearmotors and reducers are the main product type for 13 suppliers, while there are nine manufacturers with the highest sales proportion of heavy-duty gearboxes and eight vendors with the highest proportion of sales of planetary geared products. There are also manufacturers that solely focus on light-duty or planetary geared products.

This, to some extent, also reflects the market size of the three product categories. Light-duty gearmotors and gearboxes are the largest product category, accounting for approximately 56% of the global market sales in 2024. Industrial gearboxes rank second, accounting for about 26%, and planetary reducers and gearmotors account for approximately 18%.

The balance of product sales varies widely among the top 30 vendors in the global geared motors and industrial gears market

In terms of market concentration, light-duty gearmotors and gearboxes have a relatively high market share compared to other products. Affected by the dominant position of leading enterprises in the market, the top 30 manufacturers account for approximately 86% of total sales, higher than 85% for industrial gearboxes and 76% for planetary products.

Final thoughts

In recent years, due to continuous improvements in industrial automation, demand for high-performance and high reliability geared motors and industrial gearboxes has been increasing. On the supply side, the rise of emerging markets, such as China and India in the Asia-Pacific region has spurred the rapid growth of local gearbox enterprises. Consequently, this has led to heightened market competition in these regions. In the context of increasingly severe product homogenisation, global leading vendors are attempting to enhance differentiation to maintain their business in these regions. However, notably, several gearbox manufacturers from China and India have entered the list of the world’s top 30 gearbox manufacturers recently, leveraging their strong domestic market presence.

Looking ahead, global leading gearbox manufacturers will maintain their competitive edge in aspects like product reliability and reputation. Meanwhile, the development of emerging markets, downstream industries, and automation product technologies may bring new changes to the market landscape.

-----------------------

About the author:

Shirly Shu, Principal Analyst, Interact Analysis, has worked across multiple industry sectors in her 10+ year career, conducting projects requiring primary and secondary research, as well as quantitative and qualitative analysis. She’s primarily focused on Industrial Automation topics including motion and industrial controls.

Related Stories

Machine Tools & Accessories

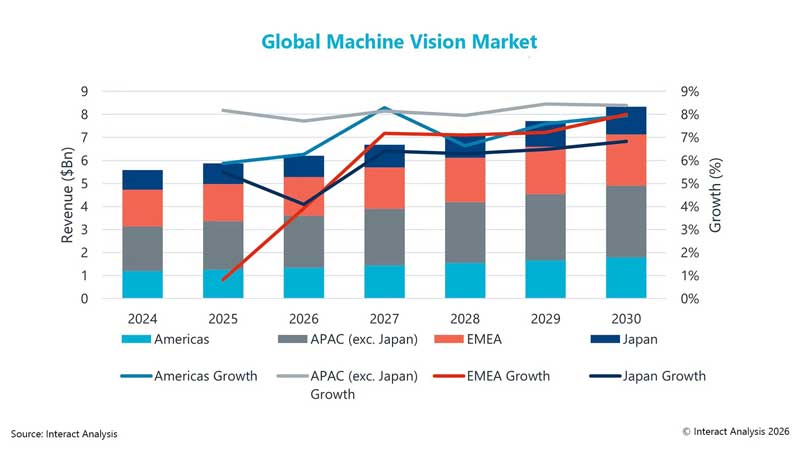

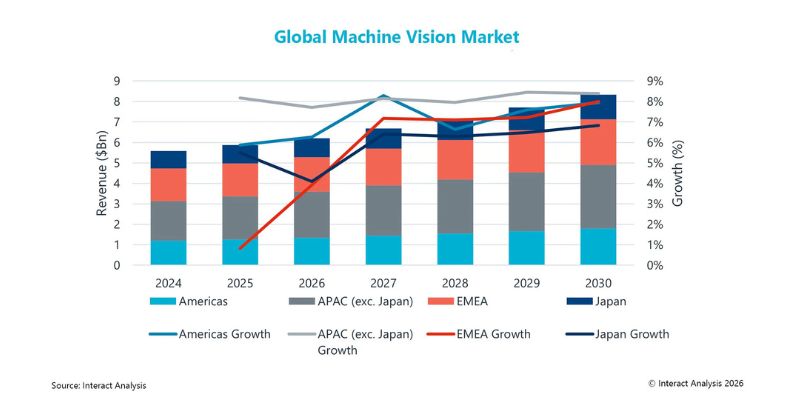

Machine vision market set to reach $8.3bn by 2030: Interact Analysis

Machine vision is set for steady growth, driven by 3D cameras, vision software and logistics automation, as demand for precision inspection rises across industries despite tariff pressures

Read moreSmart Manufacturing

Machine vision industry will reach $8.3bn in 2030: Interact Analysis

Interact Analysis says machine vision grew 5.2 per cent in 2025 and is forecast to expand 7.2% annually to $8.3 billion by 2030, driven by 3D cameras, software and logistics automation.

Read moreSmart Manufacturing

Is on-premise warehouse software making a comeback?

Rising AI workloads, cloud cost concerns, cybersecurity risks and data sovereignty requirements are prompting warehouse software buyers to reassess on-premise deployments, even as cloud remains the ..

Read moreRelated Products

Compact Fmc - Motorum 3048tg With Fs2512

INDUSTRIAL AUTOMATION & TECHNOLOGY CONSULTANCY

Meiban Engineering Technologies Pvt Ltd offers a wide range of Compact FMC - Motorum 3048TG with FS2512.

Digital Colony Counter

INDUSTRIAL AUTOMATION & TECHNOLOGY CONSULTANCY

Rising Sun Enterprises supplies digital colony counter.

Robotic Welding SPM

INDUSTRIAL AUTOMATION & TECHNOLOGY CONSULTANCY

Primo Automation Systems Pvt. Ltd. manufactures, supplies and exports robotic welding SPM.

latest News

Subscribe to iNoW

For Industry News on WhatsApp, Give a Miss Call on: +91 84228 74016