Schedule a Call Back

Bank GNPAs may touch low of 4% by FY24; MSMEs remain a concern area

Industry News

Industry News- Sep 29,22

Gross non-performing assets (GNPAs) of corporate segment is likely to fall below 2% next fiscal from a peak of 16% as on March 31, 2018; GNPAs of MSME (micro, small and medium enterprises) segment may rise to 10-11% by FY24 from approximately 9.3% as on March 31, 2022, says CRISIL Ratings.

Mumbai

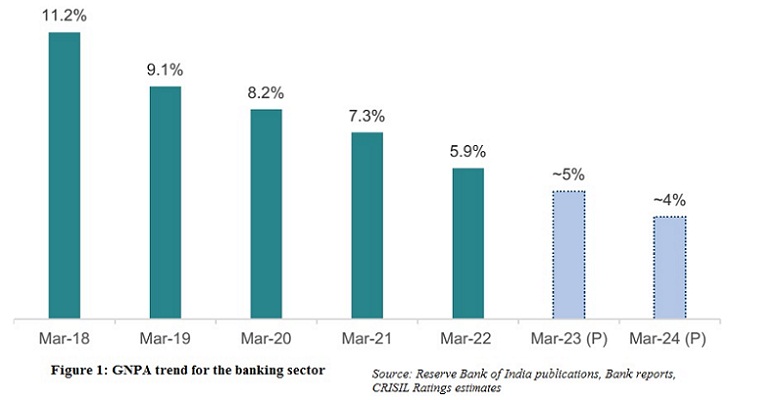

Gross non-performing assets (GNPAs) of banks — a key indicator of asset quality — is expected to improve 90 basis points (bps) to approximately 5% this fiscal on-year, and another 100 bps to a decadal low of about 4% by March 31, 2024 (refer the Figure 1), riding on post-pandemic economic recovery and higher credit growth, according to CRISIL Ratings.

The asset quality of the banking sector will also benefit from the proposed sale of NPAs to the National Asset Reconstruction Company Ltd (NARCL).

That said, not all segments will perform equally well. The biggest improvement will be in the corporate segment, where gross NPAs is seen falling below 2% next fiscal from a peak of 16% as on March 31, 2018.

Krishnan Sitaraman, Senior Director and Deputy Chief Ratings Officer, CRISIL Ratings, commented, “The steady improvement in corporate asset quality is clearly reflected in leading indicators such as the credit quality of bank exposures. A CRISIL Ratings study of large exposures of banks, constituting more than half of corporate advances, shows the share of high-safety1 exposures has increased to 77% as on March 2022 from 59% in March 2017, while exposure to sub-investment grade companies more than halved to 7% versus 17%.”

This asset quality improvement in the corporate segment follows a significant clean-up done of bank books in recent years, and strengthened risk management and underwriting. This has also led to increased preference for borrowers with better credit profiles.

The deleveraging and strengthening of India Inc balance sheets also helped. This is reflected in the CRISIL Ratings credit ratio (upgrades to downgrades), which touched 5.04 in the second half of last fiscal. The trend of upgrades comfortably outnumbering downgrades should continue over the medium term.

With much of the stress in the corporate loan book already recognised and better quality of incremental lending, restructuring for this segment was low at about 1%, covering only a few corporate groups. Mechanisms such as the Insolvency and Bankruptcy Code have also supported recoveries and increased credit discipline among borrowers.

Gross NPA in the MSME (micro, small and medium enterprises) segment, which suffered the most during the pandemic, may rise to 10-11% by March 2024 from approximately 9.3% as on March 31, 2022. While relief measures did help contain asset quality deterioration last fiscal, the segment saw the most restructuring at 6% compared with 2% for the overall banking sector. About a fourth of these accounts could potentially slip into NPAs.

The retail segment remains resilient and gross NPAs are expected to remain range-bound at 1.8-2.0% over the medium term. While the impact of increase in interest rates and inflationary pressure on individual borrowers’ cash flows will need to be monitored, almost half of the retail loans are home loans, where borrowers have relatively better credit profiles. While segments such as unsecured loans may see some pressure, overall retail asset quality is expected to stay within expected bounds. Agriculture segment gross NPAs is seen flat at 9-10% following another year of reasonably normal monsoon and harvest.

Subha Sri Narayanan, Director, CRISIL Ratings, commented, “We expect slippages to trend 50 bps lower at approximately 2% for fiscal 2024 versus 2.5% last fiscal as the economy stabilises. This should support asset quality metrics even as the pace of write-offs, which contributed almost 60% to the reduction in gross NPAs in the past three fiscals, and large-ticket resolutions decelerate. Our base-case estimate factors in part-sale of legacy corporate loan NPAs to the NARCL, which should snip reported gross NPAs by about 50 bps.”

Over the medium term, to avoid a repeat of past asset-quality challenges, it is important that banks don’t relax their credit underwriting standards while focussing on faster growth.

Related Stories

Smart Manufacturing

Gujarat Unveils New Industrial Policy 2026 to Drive Manufacturing, Innovation

Viksit Gujarat Industrial Policy 2026 identifies 21 high-growth thrust sectors, with special emphasis on emerging industries such as robotics, drones, footwear, toy manufacturing, and sports equipme..

Read moreAutomation & Robotics

Transforming India’s SMEs: From Domestic Players to Global Competitors

India’s manufacturing ambitions hinge on SMEs scaling from domestic strength to global competitiveness. Capability, quality, finance and trust will determine how effectively they integrate into gl..

Read moreElectrical & Electronics

Electronics, automation to drive India’s manufacturing growth: V Sriram Kumar

With India accelerating its push in electronics and semiconductor manufacturing, building a robust, self-reliant ecosystem has become critical. In this interaction with V. Sriram Kumar, CEO, ELCIA o..

Read moreRelated Products

Heavy Industrial Ovens

INDUSTRIAL SUPPLIES

Hansa Enterprises offers a wide range of heavy industrial ovens.

High Quality Industrial Ovens

INDUSTRIAL SUPPLIES

Hansa Enterprises offers a wide range of high quality industrial ovens. Read more

Hydro Extractor

INDUSTRIAL SUPPLIES

Guruson International offers a wide range of cone hydro extractor. Read more

latest News

Subscribe to iNoW

For Industry News on WhatsApp, Give a Miss Call on: +91 84228 74016